C++ / Trading Systems Project

C++ Matching Engine

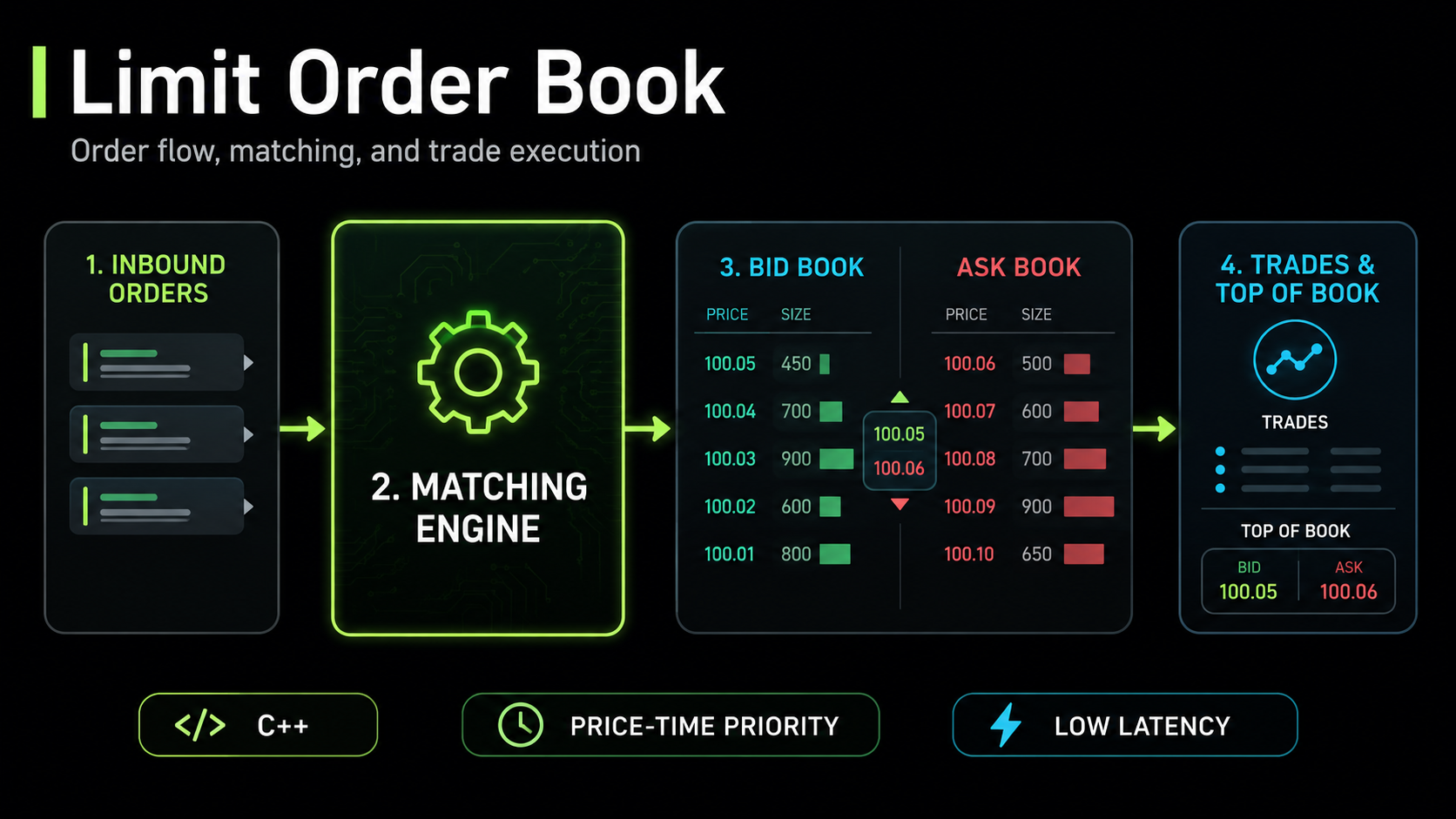

A deterministic limit order book and matching engine in C++ that models price-time priority, partial fills, cancellations, seeded order flow, and measurable engine throughput.

Key Features

- Price-time priority matching with best price first

- FIFO execution within each price level

- Partial fills across resting liquidity

- Cancellation support for resting orders

- Deterministic simulation using a fixed random seed

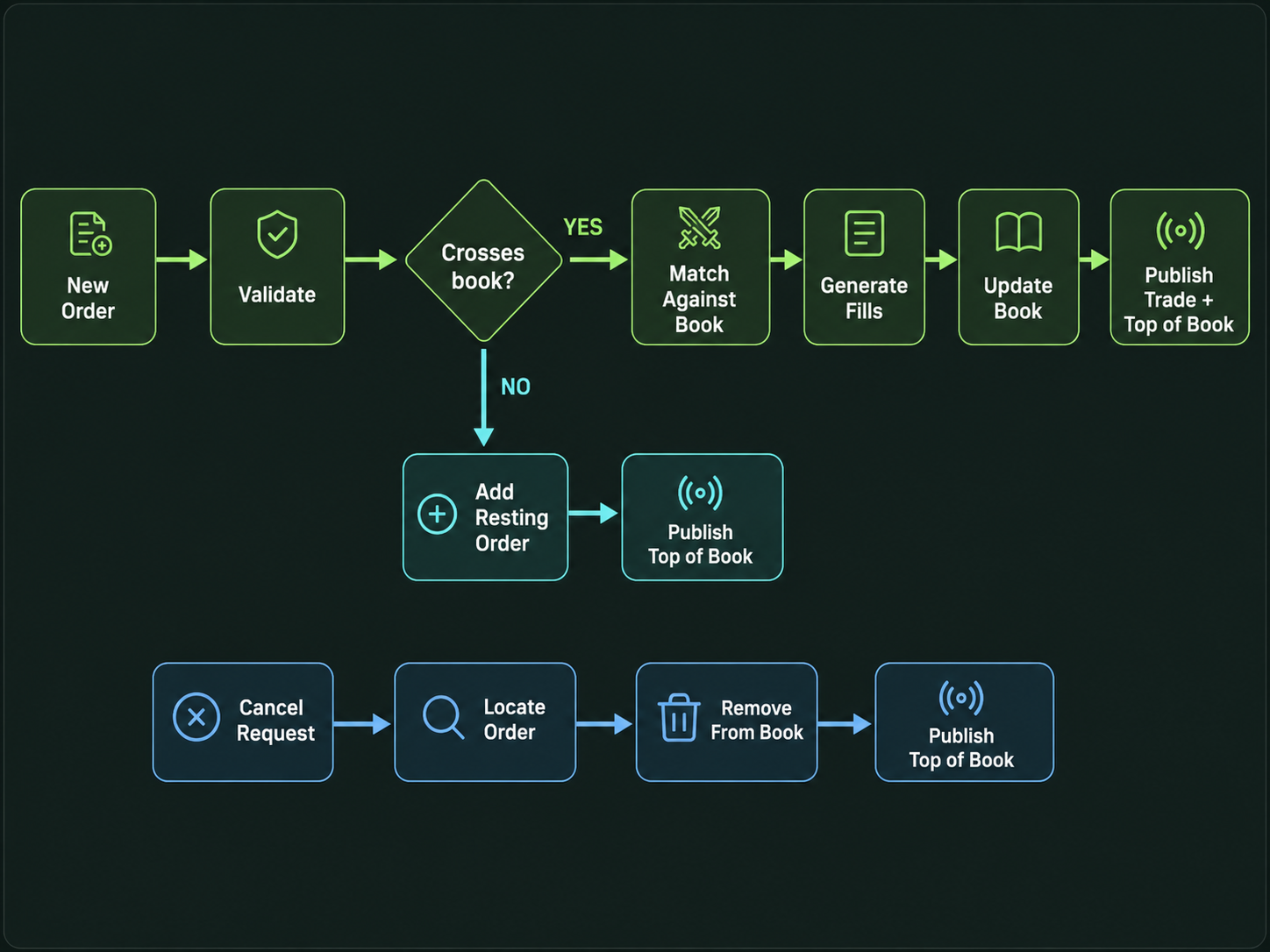

Matching Flow

- Incoming buy orders cross against the best ask while price permits

- Incoming sell orders cross against the best bid while price permits

- Fill quantity is the minimum of incoming and resting quantity

- Fully filled resting orders are removed from the front of the queue

- Unfilled incoming quantity rests at its limit price

Architecture

- Bid side uses descending ordered price levels

- Ask side uses ascending ordered price levels

- Each price level stores orders in FIFO queues

- Simulator generates seeded add and cancel events

- Engine reports trade count, volume, spread, average trade size, and throughput

Example Engine Output

=== SIMULATION CONFIG === Seed: 42 Events: 100000 === SIMULATION SUMMARY === Add Orders Processed: 80103 Cancel Attempts: 19897 Successful Cancels: 5009 === TOP OF BOOK === Best Bid: 95 Best Ask: 96 Final Spread: 1 === ENGINE METRICS === Trades Executed: 58189 Total Traded Volume: 177043 Average Trade Size: 3.042551 Elapsed Time: 0.051799s Throughput: 1,930,535.47 events/sec Goal: model core trading-engine behavior while keeping correctness, determinism, and measurable system performance visible.

Highlights

- Built deterministic C++ limit order book with price-time priority matching

- Implemented partial fills, resting order insertion, and cancellation support

- Modeled bid and ask books with sorted price levels and FIFO queues

- Simulated 100K seeded order events for reproducible benchmark runs

- Tracked trades executed, traded volume, final spread, average trade size, and throughput

- Separated matching logic from simulation flow for cleaner system structure

- Documented future paths for indexed cancellation, cache-friendly storage, and multi-instrument support

Execution Model

- Best price is matched first

- FIFO preserves time priority

- Partial fills carry remaining quantity forward

- Spread is derived from best ask minus best bid

What I Learned

- Correct matching rules matter before raw speed

- Deterministic seeds make performance easier to reason about

- Cancellation lookup becomes a real scaling bottleneck

- Data structure choices shape both clarity and throughput

Tech Stack

- C++17

- CMake

- std::map and std::deque

- chrono benchmark timing

- Seeded random simulation